November – Be thankful

What started as a bumpy ride for the S&P 500 finally ended the month slightly positive, following a shortened last week rally. In fact everything rallied, commodities (ex oil), bonds, stocks, bitcoin…now that’s something to be thankful for!

Indeed, growing fears of an AI bubble caused the US stock market to go down over 5% earlier in the month. But then investors, too often guilty of having the short-term memory of a goldfish, forgot all about it and instead focused on any positive signs they found to go back into risk-on mode. The positive signs came in the form of a better than feared job report (though still deteriorating) coming out and the growing expectation of a December rate cut. We are also worried about the current tech stocks valuations and the fragility of the sector (more on that in our graph of the month section).

Data source : Bloomberg

The faith in US AI stocks was somewhat shaken this month, with shares of companies such as Nvidia, Oracle and Palantir taking double digit losses. However, it seems investors just moved money out of technology and into other sectors such as healthcare (up about 9%) and Black Friday friendly companies, hoping shoppers took full advantage of the available bargains to boost earnings come year end reporting period.

With the longest shutdown in US history finally over, government employees can resume their work and those working for the Labor Statistics Bureau can once again publish key data for economists and the Fed, bar the one month gap. But estimates point to weak but not as bad as expected figures. Investors will grab on anything they can to fuel their optimism and “not as bas as expected” is enough to be positive. Non-government figures such as PMI also point to the same conclusion. Consumers, however, do not share the same optimism, with surveys such as the Michigan Consumer Sentiment coming out as the second worst month on record after June 2022.

On the other side of the Atlantic, Europe does what we have been accustomed to, which is slow growth, unexciting job data, mediocre outlook. A lot of hope is being placed on a Ukraine peace deal, but we have yet to see sincere intentions from the Russian side and the US flip flopping on the issue like a borderline personality disorder patient.

In Asia, Japan ended the month in negative territory in part due to a higher than expected inflation figure (3%) and the prospect that the Bank of Japan could raise interest rates to combat an inflation rate that has been above target since Covid. However, the negative GDP growth of the country is limiting the range of actions the BoJ can take to avoid a recession.

Chinese stocks also ended the month in negative territory following figures placing factory activity in contraction territory and the lack of enthusiasm for technology stocks, a quarter of which, make up the China A shares index.

Our summary recommendations

This month gave us another short-lived opportunity to strike interesting defensive structured products. As we’ve repeated in previous months, at current market levels, we feel a lot more comfortable deploying cash in a defensive manner and provide clients with a nice layer of protection should a correction take place.

Chart of the month

You have now heard countless times from various sources that technology stocks are very expensive, many call it a bubble, some fear it will burst. The million-dollar question is when?

We believe that we are seeing the first cracks on the golden egg. Not from equity valuations, but from the credit side.

As you know, AI research and development is a high cash burning endeavor requiring an extravagant amount of investments, often financed through debt. On the other hand, return on investment is hardly materializing and hard to quantify at this stage.

Furthermore, many of the firms involved in the AI race are intertwined through a circular flow of partnerships, service agreements, investments, etc…meaning if one breaks, the domino effect will be inevitable. This is not unlike how the banks and insurance companies were so connected, leading into the great financial crisis of 2008.

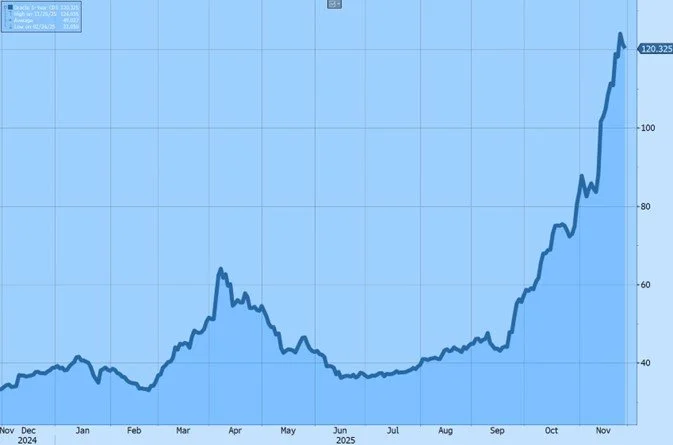

Below is a graph of the Oracle Corporation’s 5-year CDS (Credit Default Swap) over the past year. The CDS is a measure of the perceived credit riskiness of a company and Oracle’s is shooting through the roof. Their total debt to equity is now above 500% and investors are placing a big premium on owning their debt.

As a company working in database management, cloud computing/infrastructure as well as software, they are at the heart of the big tech and AI. Most of the big tech companies are still cash rich, but for those heavily relying on debt like Oracle, a debt trap could be the catalyst to the next major crisis. Rest assured though, none of our clients own Oracle debt.

Source: Bloomberg

Disclosures

This document has been issued by Stork Capital, registered with the Swiss Association of Asset Managers, and licensed by FINMA.

Offering Documents. This material is provided at your request for informational purposes only and is not intended as an offer, a solicitation of an offer, to buy, sell or carry out any transaction on investment instruments or other specific product, it only contains selected information with regards to Stork Capital’s services. The analysis and information contained herein do not constitute a personal recommendation or consider the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, however, Stork Capital cannot guarantee the accuracy of such content, ensure its completeness, or warrant that such information has not or will not change.

Prior to any investment, prospective investors should carefully read the latest offering documentation, including but not limited to the fund’s prospectus which contains inter alia a comprehensive disclosure of applicable risks. The relevant constitutional and offering documents are available free of charge at Stork Capital’s principal office.

Risk Information and Potential Loss. Financial advisers generally suggest a diversified portfolio of investments. The funds described herein do not represent a diversified investment by themselves. This material does not constitute investment advice and should not be used as the basis for any investment decision. This material does not purport to provide any legal, tax or accounting advice. Prospective investors should consult their financial and tax adviser before investing in order to determine whether an investment would be suitable for them.

Any investor or prospective investor should be aware of the risks inherent in trading activity, such as but not limited to currency risk, interest-rate risk, market risk, insolvency risk, and is aware that trading can be very speculative and may result in losses as well as profits. Therefore, an investor should only invest if he/she has the necessary financial resources to bear a complete loss of this investment.

Portfolio Allocations. This material contains information that pertains to past performance or is the basis for previously-made discretionary investment decisions. The value of investments may fall as well as rise and investors may not get back the amount they invested. Thus, past performance does not necessarily provide any guarantee of future results. Accordingly, this information should not be construed as a current recommendation, research or investment advice. It should not be assumed that any investment decisions shown will prove to be profitable, or that any investment decisions made in the future will be profitable or will equal the performance of investments discussed herein. Any mention of an investment decision is intended only to illustrate our investment approach and/or strategy, and is not indicative of the performance of our strategy as a whole. Any such illustration is not necessarily representative of other investment decisions.

Portfolio holdings and/or allocations shown above are as of the date indicated and may not be representative of future investments. The holdings and/or allocations shown may not represent all of the portfolio's investments. Future investments may or may not be profitable.

Intended Recipients. This material and any information contained therein shall only be for the personal use of the intended recipient and shall not be redistributed to any third party, unless Stork Capital or the source of the relevant market data gives their approval. This material is not directed to any person in any jurisdiction where (on the grounds of that person’s nationality, residence or otherwise) such documents are prohibited. In particular, neither this document nor any copy thereof may be sent, taken into or distributed in the United States or to any US person.

Disclaimer of Endorsement. References in these discussion materials to any specific manager, service provider, vendor, market, index, financial procedure, process, resources, or commercial services do not constitute nor imply its endorsement, recommendation, or favour by Stork Capital. Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Stork Capital to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice. The website links provided are for your convenience only and are not an endorsement or recommendation by Stork Capital of any of these websites or the products or services offered. Stork Capital is not responsible for the accuracy and validity of the content of these websites.

Investment Risks. Risks vary by the type of investment. For example, investments that involve futures, equity swaps, and other derivatives, as well as non-investment grade securities, give rise to substantial risk and are not available to or suitable for all investors. We have described some of the risks associated with certain investments below and, in certain cases, earlier in this presentation. Additional information regarding risks may be available in the materials provided in connection with specific investments. You should not enter into a transaction or make an investment unless you understand the terms of the transaction or investment and the nature and extent of the associated risks. You should also be satisfied that the investment is appropriate for you in light of your circumstances and financial condition.

Alternative Investments. Private investment funds and hedge funds are subject to less regulation than other types of pooled vehicles. Alternative investments may involve a substantial degree of risk, including the risk of total loss of an investor’s capital and the use of leverage, and therefore may not be appropriate for all investors. Liquidity may be limited. Investors should review the Offering Memorandum, the Subscription Agreement and any other applicable disclosures for risks and potential conflicts of interest. Alternative Investments may be subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments may not be required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

Real Estate. Investments in real estate involve additional risks not typically associated with other asset classes, such as sensitivities to temporary or permanent reductions in property values for the geographic region(s) represented. Real estate investments (both through public and private markets) are also subject to changes in broader macroeconomic conditions, such as interest rates.

The sole place of jurisdiction for all disputes arising out of or in connection with this material and/or the present disclaimer and/or to the use of this material is Geneva, Switzerland, and it shall be exclusively governed by and construed in accordance with Swiss law.