April – Strait up goes inflation

Two months after the beginning of the offensive against Iran by Israel and the United States and the fallout in the entire Middle East region, no exit strategy or durable peace plan has emerged and as a result, uncertainty remains. At least for now, the truce is holding.

One thing we know for certain is the direct impact on the oil prices and the resulting jump in inflation. And the inflation story is not over, other sectors will certainly be impacted too with a slight delay. Think food costs due to fertilizers being a byproduct of oil/gas, packaging with plastics being derived from oil, the transportation industry, pharmaceuticals, etc…humanity’s bad romance with oil is deep.

As a result, multiple central banks and institutions such as the IMF have reviewed their growth expectations downward. For example, the European Central Bank revised GDP growth for the Euro area downward by 0.3% for 2026. The IMF revised global growth down from 3.3% to 3.1% for 2026 and inflation up to 4.4% from 3.8%. These figures are typically reviewed on a quarterly basis and will inevitably change as the war evolves for better or for worse.

Countries have an opportunity to help mitigate the damage through fiscal measures to households and industries having a hard time absorbing the sudden supply shock. As each country faces a different level of dependence on the Middle East, a coordinated action is unlikely.

More surprisingly, the markets had an outstanding month of April. Japan and the US are up in the teens, while the rest of the world is up in a more measured way (World index up 9.59%). It is incomprehensible that markets have their best month in years in a context where we are just a spark away from an escalation in the conflict. The rally is led, unsurprisingly, by the technology sector, which accounts for over half the performance. Excellent corporate earnings and resilience to oil shocks are also part of the explanation.

In the US, other elements raise concerns. The job market is cooling down on multiple fronts. The immigration policy is impacting the supply side, while demand is reduced by the impact of AI and the prior over-hiring that took place following COVID. Because the Fed has a double mandate to ensure full employment and price stability (inflation target of 2%), the direction it will take interest rates is now unsure. A slowing economy and job market would warrant lowering interest rates, while a rise in inflation would call for a rate hike. To make things more complex, in the middle of all this, Kevin Warsh, the presumptive nominee, should take over the Fed chairmanship in May. In contradiction, despite the growth outlook being reduced, the PMIs are up further in expansion territory in both services and manufacturing.

In Europe, where inflation had been subdued to within target levels, it is now rebounding to 3%. Fortunately, the ECB, being ahead of the US in the interest rate cutting cycle, has more capacity to raise interest rates if needed. European indices being much less tech heavy (mid-teens VS mid-thirties in the US) and much more “old economy” such as financials and industrials, the rebound wasn’t as impressive. Not only was Europe’s GDP growth outlook cut, PMIs are in contraction territory, leaving us feeling pessimistic. At least for now the job market and consumption remain strong.

China kept relatively muted and on the sideline throughout the recent events, but their economy hasn’t. On the contrary, China posted a GDP growth of 5% for Q1 and the IMF revised upward their growth expectations for the year. This is very surprising as we keep hearing that they were so dependent on Venezuelan and Iranian oil, as major input in their economy.

House View

With the uncertainty brought forth by geopolitical conflicts that are far from being resolved (or not, we just don’t know), we remain prudent. Our defensive stance helped a lot of clients sleep well at night in March when, at its worst, clients with a balanced profile had a flat performance. In April, we have not rebounded as much, but we feel that April performance was irrational. We remain therefore rather defensive and ready to seize an opportunity to increase risk or capitalize on volatility.

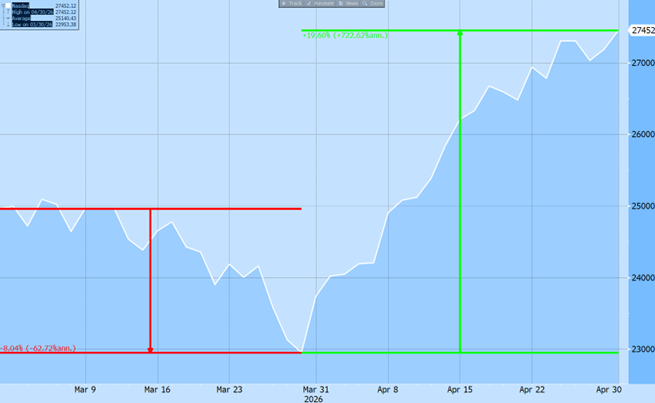

Chart of the month

The chart of the month shows the performance of the famous US tech index, the Nasdaq. We want to highlight the volatility and irrationality happening at the moment.

From the close of the market prior to the war until the lowest point, the index lost over -8%. From that point until end of April, it rallied over +19%. Should the war resume, it is feasible to see it drop once again to the march lows.

Source: Bloomberg

Disclosures

This document has been issued by Stork Capital, registered with the Swiss Association of Asset Managers, and licensed by FINMA.

Offering Documents. This material is provided at your request for informational purposes only and is not intended as an offer, a solicitation of an offer, to buy, sell or carry out any transaction on investment instruments or other specific product, it only contains selected information with regards to Stork Capital’s services. The analysis and information contained herein do not constitute a personal recommendation or consider the particular investment objectives, investment strategies, financial situation and needs of any specific recipient. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, however, Stork Capital cannot guarantee the accuracy of such content, ensure its completeness, or warrant that such information has not or will not change.

Prior to any investment, prospective investors should carefully read the latest offering documentation, including but not limited to the fund’s prospectus which contains inter alia a comprehensive disclosure of applicable risks. The relevant constitutional and offering documents are available free of charge at Stork Capital’s principal office.

Risk Information and Potential Loss. Financial advisers generally suggest a diversified portfolio of investments. The funds described herein do not represent a diversified investment by themselves. This material does not constitute investment advice and should not be used as the basis for any investment decision. This material does not purport to provide any legal, tax or accounting advice. Prospective investors should consult their financial and tax adviser before investing in order to determine whether an investment would be suitable for them.

Any investor or prospective investor should be aware of the risks inherent in trading activity, such as but not limited to currency risk, interest-rate risk, market risk, insolvency risk, and is aware that trading can be very speculative and may result in losses as well as profits. Therefore, an investor should only invest if he/she has the necessary financial resources to bear a complete loss of this investment.

Portfolio Allocations. This material contains information that pertains to past performance or is the basis for previously-made discretionary investment decisions. The value of investments may fall as well as rise and investors may not get back the amount they invested. Thus, past performance does not necessarily provide any guarantee of future results. Accordingly, this information should not be construed as a current recommendation, research or investment advice. It should not be assumed that any investment decisions shown will prove to be profitable, or that any investment decisions made in the future will be profitable or will equal the performance of investments discussed herein. Any mention of an investment decision is intended only to illustrate our investment approach and/or strategy, and is not indicative of the performance of our strategy as a whole. Any such illustration is not necessarily representative of other investment decisions.

Portfolio holdings and/or allocations shown above are as of the date indicated and may not be representative of future investments. The holdings and/or allocations shown may not represent all of the portfolio's investments. Future investments may or may not be profitable.

Intended Recipients. This material and any information contained therein shall only be for the personal use of the intended recipient and shall not be redistributed to any third party, unless Stork Capital or the source of the relevant market data gives their approval. This material is not directed to any person in any jurisdiction where (on the grounds of that person’s nationality, residence or otherwise) such documents are prohibited. In particular, neither this document nor any copy thereof may be sent, taken into or distributed in the United States or to any US person.

Disclaimer of Endorsement. References in these discussion materials to any specific manager, service provider, vendor, market, index, financial procedure, process, resources, or commercial services do not constitute nor imply its endorsement, recommendation, or favour by Stork Capital. Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Stork Capital to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice. The website links provided are for your convenience only and are not an endorsement or recommendation by Stork Capital of any of these websites or the products or services offered. Stork Capital is not responsible for the accuracy and validity of the content of these websites.

Investment Risks. Risks vary by the type of investment. For example, investments that involve futures, equity swaps, and other derivatives, as well as non-investment grade securities, give rise to substantial risk and are not available to or suitable for all investors. We have described some of the risks associated with certain investments below and, in certain cases, earlier in this presentation. Additional information regarding risks may be available in the materials provided in connection with specific investments. You should not enter into a transaction or make an investment unless you understand the terms of the transaction or investment and the nature and extent of the associated risks. You should also be satisfied that the investment is appropriate for you in light of your circumstances and financial condition.

Alternative Investments. Private investment funds and hedge funds are subject to less regulation than other types of pooled vehicles. Alternative investments may involve a substantial degree of risk, including the risk of total loss of an investor’s capital and the use of leverage, and therefore may not be appropriate for all investors. Liquidity may be limited. Investors should review the Offering Memorandum, the Subscription Agreement and any other applicable disclosures for risks and potential conflicts of interest. Alternative Investments may be subject to less regulation than other types of pooled investment vehicles such as mutual funds. Alternative Investments may impose significant fees, including incentive fees that are based upon a percentage of the realized and unrealized gains and an individual’s net returns may differ significantly from actual returns. Such fees may offset all or a significant portion of such Alternative Investment’s trading profits. Alternative Investments may not be required to provide periodic pricing or valuation information. Investors may have limited rights with respect to their investments, including limited voting rights and participation in the management of such Alternative Investments.

Real Estate. Investments in real estate involve additional risks not typically associated with other asset classes, such as sensitivities to temporary or permanent reductions in property values for the geographic region(s) represented. Real estate investments (both through public and private markets) are also subject to changes in broader macroeconomic conditions, such as interest rates.

The sole place of jurisdiction for all disputes arising out of or in connection with this material and/or the present disclaimer and/or to the use of this material is Geneva, Switzerland, and it shall be exclusively governed by and construed in accordance with Swiss law.